As markets widely expected, the Federal Reserve finally joined the global policy easing cycle with a 50 basis point (bps) rate cut this week, bringing its target rate down to a range of 4.75 bps to 5.00 bps from 5.25 bps to 5.50 bps. While there was an unusual level of uncertainty heading into this week’s policy meeting with respect to the size of the cut—25 or 50 bps—our expectation was for 50 bps, and therefore we think the Fed made the right call here.

Back at the July meeting, according to the minutes, there was already an open discussion among policymakers of whether to cut rates. Since then, inflationary pressures have only cooled further while the two payrolls reports released have been much softer than the Bloomberg consensus expected. While Fed Chair Jerome Powell during his press conference wouldn’t go so far as to characterize the larger rate cut this week as an effort to play catch up to a labor market that may be cooling faster than policymakers expected, we would.

But whether this is a classic case of “too little, too late” remains to be seen, in our view—in both 2001 and 2007 the Fed kicked off easing cycles with outsized rate cuts, which, of course, are not great periods to be benchmarked to. We believe the Fed’s proactive decision this week, at a time when policymakers could have easily justified a standard 25 bps cut, should support prospects of a so-called soft economic landing, while reducing risks of a hard landing. But that, of course, remains highly uncertain, and highly dependent on how the economic data develops.

Cutting isn’t easy

Given that the Fed chose to cut rates this week by more than consensus surveys had expected, and that its own revised rate projections also show more rate cuts in the pipeline than anticipated, investors may harbor some concerns that the Fed is getting ahead of itself, and that more aggressive rate cuts could reignite inflationary pressures.

While the Fed’s headline policy rate garners much of the attention, everything is relative. What we believe actually matters in terms of economic activity, inflation, and employment is the level of real interest rates—or the Fed’s policy rate adjusted for inflation.

Real rates peaked around three percent in recent months—with a fed funds rate of 5.5 bps and a headline personal consumption expenditures (PCE) inflation rate of 2.5 bps as of the latest reading in July—a level consistent with those reached in recent decades. But those points also tended to be followed by recessions.

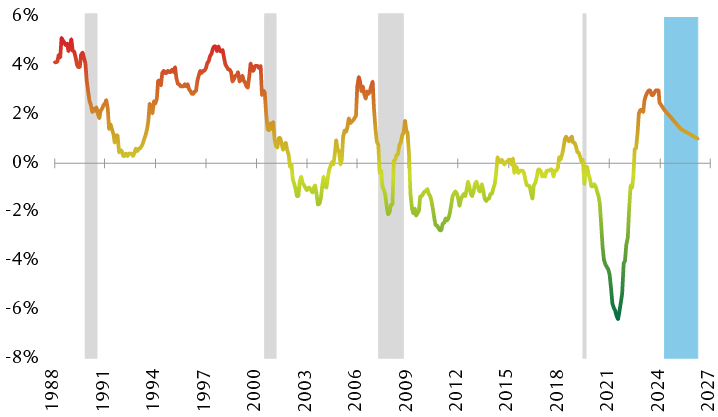

Even with cuts, real rates likely to remain elevated

Real federal funds rate (rate less PCE inflation)

The line chart shows the Federal Reserve’s real policy rate, or the official policy interest rate adjusted for inflation, since 1988, and the projected rate through the end of 2026. The real rate rose sharply from a low of -6.4% in April 2022 and peaked around 3% in July. The Fed’s rate and inflation forecasts suggest it is likely to fall only gradually in the future, reaching a level of approximately 1% at the end of 2026.

Source - RBC Wealth Management, Bloomberg; real rate forecast based on Federal Reserve Summary of Economic Projections for PCE inflation and federal funds rate

The Fed’s updated Summary of Economic Projections shows that the central bank expects to take the upper bound of its target range down to 4.50 percent by the end of this year, to 3.50 bps in 2025, and to 3.00 percent in 2026. Policymakers also expect inflation to fade back to target over that horizon, which would leave real rates at a still relatively high level of 1.00 bps (3.00 bps fed funds rate minus the 2.00 bps target inflation rate).

At the same time, if we think the Fed’s moves could shore up the economic outlook, we have to acknowledge that a slightly better economic outlook could also mean that inflationary progress could slow.

Follow the leader again?

Back in 2023, and amid still high uncertainty that inflation would cool to the point to allow Fed rate cuts in 2024, we looked to emerging markets for clues. The general thinking is that inflation tends to be more of a problem for emerging markets, and therefore the central banks of those nations must be more attuned to inflationary risks.

For example, the Central Bank of Brazil began raising rates in early 2021, about one year before developed market central banks followed suit. In the summer of 2023, the Central Bank of Brazil began cutting rates as inflationary pressures dropped. If that same lead time held, then it seemed reasonable that developed market central banks could be easing by this summer, which they have.

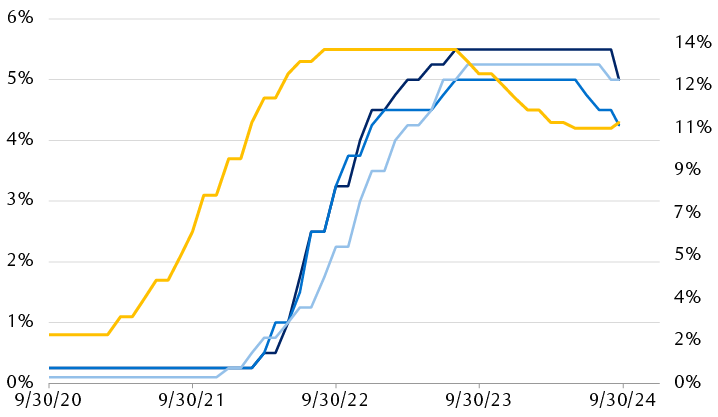

As central banks in developed markets begin to cut rates, some emerging markets pivot back to hikes

The line chart compares the evolution of central bank policy rates in the U.S., Canada, the United Kingdom, and Brazil from September 2020 through September 19, 2024. The Bank of Brazil was both the first to begin raising rates and the first to begin cutting rates. While other central banks are now cutting, the Bank of Brazil raised rates in September 2024.

Source - RBC Wealth Management, Bloomberg

So, and with that in mind, just as the Fed delivered a 50 bps rate cut on Wednesday, the Central Bank of Brazil moved to raise its policy rate by 25 bps, its first rate hike since it began lowering rates in August 2023. Policymakers in Brazil cited growing risks around higher inflation forecasts as one reason to add back some policy restrictiveness, and noted that more rate hikes could be on the table.

To be crystal clear, we do not expect a second wave of inflation in the U.S. or globally, but we always have to be cognizant of potential risk factors. And if we used emerging market central banks as leading indicators for rate cuts, we would be remiss if we didn’t keep one eye on how other easing cycles have transpired.

That said, one reason that upside risks to inflation have returned to Brazil has been a weaker currency as the central bank has cut rates at a time when the Fed delayed them. Therefore, we think Fed rate cuts should help to ease currency pressures in Brazil, and therefore inflationary pressures as well—so this may not be an explicit warning sign on resurgent inflationary risks for developed markets.

The here and now

The proactive decision by the Fed this week should help to shore up the economic outlook, and we are encouraged that the Fed has chosen to do so when it has historically been too reactive, and therefore often too late in dialing back monetary policy restrictiveness.

Plenty of economic and policy-related uncertainty will undoubtedly remain. But we believe the strong start out of the rate cut gates by the Fed should go some ways toward staving off intermediate-term recessionary risks, or at a minimum material further weakness in U.S. labor markets.